Nearshore virtual bookkeepers are handling more of the financial back-office for US businesses than ever before — and one of the most common questions owners ask before hiring one is: can a virtual bookkeeper actually file my taxes? The short answer is: probably not on their own, but they can do most of the heavy lifting that makes tax time fast, affordable, and far less stressful. Understanding exactly where that line sits will help you build the right team at the right cost.

This guide breaks down the legal distinction between bookkeeping and tax filing, what a skilled virtual bookkeeper can prepare for your CPA, and how pairing the two roles saves most small businesses thousands of dollars a year in accounting fees. We'll also cover what to look for when hiring a virtual bookkeeper specifically to support your tax workflow in 2026.

What Does a Virtual Bookkeeper Actually Do in 2026?

A virtual bookkeeper is a remote financial professional who maintains your day-to-day accounting records — categorizing transactions, reconciling bank and credit card accounts, managing accounts payable and receivable, and producing financial statements like profit-and-loss reports and balance sheets. They work inside your accounting software (QuickBooks, Xero, FreshBooks, Wave) and keep your books accurate on a weekly or monthly cadence so nothing piles up.

What separates a great virtual bookkeeper from a basic data-entry hire is domain expertise. A bookkeeper trained specifically in your industry — whether that's real estate, e-commerce, professional services, or construction — understands the chart of accounts, the depreciation schedules, and the expense categories that matter to your CPA at year-end. If you're already using QuickBooks and wondering how that fits into a virtual hire, our breakdown of whether a virtual bookkeeper can use QuickBooks Live covers the platform compatibility questions in detail.

According to the U.S. Bureau of Labor Statistics (2024), there are over 1.7 million bookkeeping and accounting clerks employed in the United States — a role that has increasingly shifted to remote and virtual delivery models as cloud accounting software matured.

Can a Virtual Bookkeeper File My Taxes? The 2026 Legal Reality

Legally, tax filing in the United States requires specific credentials. Only a Certified Public Accountant (CPA), a licensed Enrolled Agent (EA), or a tax attorney can represent you before the IRS and sign a federal tax return on your behalf. Bookkeepers — virtual or otherwise — do not hold these credentials unless they have separately obtained one of those licenses. This is a hard regulatory line, not a capability question.

However, the line between "filing taxes" and "doing the work that makes filing possible" is where most small business owners misunderstand the split. A skilled virtual bookkeeper can complete roughly 70–80% of the total work involved in tax preparation. What they can't do is put their signature on the return or legally advise you on tax strategy.

"Most small business owners pay their CPA for work their bookkeeper should have already done. Clean books coming into tax season can cut your CPA bill by 30 to 50 percent." — Lisa Simpson, CPA and founder of The Bookkeeping Academy (2023)

The IRS explicitly defines the credentials required to prepare and sign federal tax returns, and bookkeepers are not on that list unless they hold a Preparer Tax Identification Number (PTIN) and operate under supervised conditions. If a virtual bookkeeper offers to "file your taxes" without disclosing their credentials, that is a red flag.

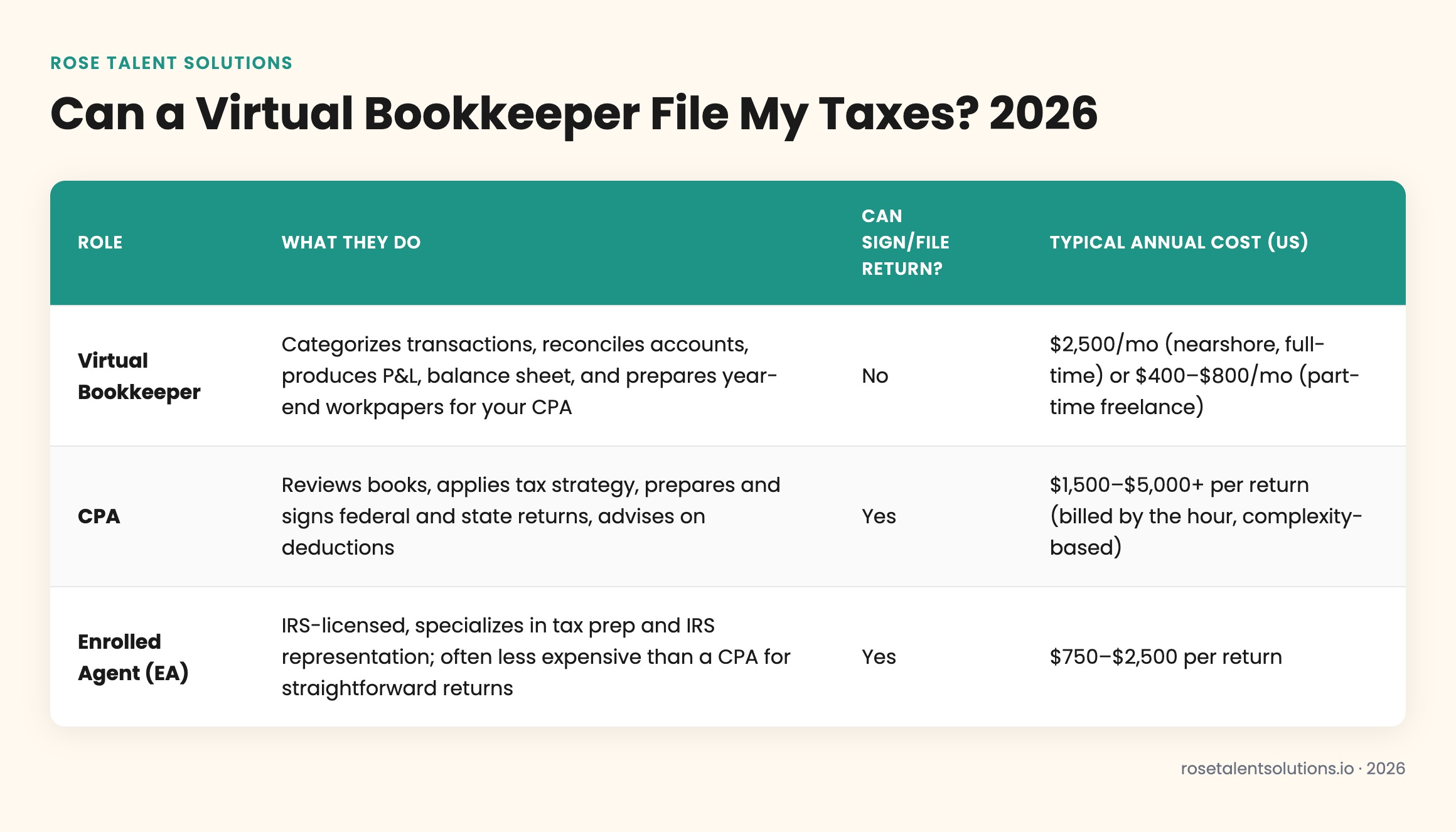

The Three Roles You Need at Tax Time — and Which One a VA Fills

| Role | What They Do | Can Sign/File Return? | Typical Annual Cost (US) |

|---|---|---|---|

| Virtual Bookkeeper | Categorizes transactions, reconciles accounts, produces P&L, balance sheet, and prepares year-end workpapers for your CPA | No | $2,500/mo (nearshore, full-time) or $400–$800/mo (part-time freelance) |

| CPA | Reviews books, applies tax strategy, prepares and signs federal and state returns, advises on deductions | Yes | $1,500–$5,000+ per return (billed by the hour, complexity-based) |

| Enrolled Agent (EA) | IRS-licensed, specializes in tax prep and IRS representation; often less expensive than a CPA for straightforward returns | Yes | $750–$2,500 per return |

What a Virtual Bookkeeper Can Prepare for Tax Season in 2026

Even though a virtual bookkeeper can't file your return, the deliverables they produce are what your CPA actually needs. A well-organized set of books can cut your CPA's hourly bill by 30–50% because the CPA spends time on strategy and compliance — not sorting through a year of uncategorized Stripe and bank transactions.

Here is what a trained virtual bookkeeper delivers ahead of tax season:

- Reconciled bank and credit card statements — every account matched to the penny, with no unexplained differences

- Categorized expense reports — every transaction mapped to the correct IRS-recognized expense category (meals, travel, home office, COGS, etc.)

- Profit & Loss statement — monthly and year-to-date, ready for your CPA to review

- Balance sheet — assets, liabilities, and equity as of December 31

- Accounts payable aging report — showing outstanding vendor invoices that may create year-end accruals

- 1099 vendor tracking — compiling W-9 information and payment totals for any contractor paid $600+ during the year, so your CPA can issue 1099-NECs on time

- Depreciation schedules — tracking fixed assets and working with your CPA on Section 179 or bonus depreciation elections

If your bookkeeper is working in Xero, they can export reports directly in formats your accountant can import. Our guide on hiring a Xero virtual bookkeeper covers how the platform's built-in advisor tools streamline this exact handoff. For cost benchmarking, our 2026 QuickBooks virtual bookkeeper cost breakdown shows what full-time versus part-time coverage actually runs.

The biggest hidden cost in small business tax prep isn't your CPA's rate — it's disorganized books handed to a CPA who then charges $200/hr to reconstruct a year of transactions your bookkeeper should have maintained all along. Clean books all year is the highest-ROI accounting investment you can make.

How Nearshore Virtual Bookkeepers Outperform Offshore Alternatives for US Tax Prep

Not all virtual bookkeepers are built for US tax workflows. A bookkeeper based 10–13 time zones away who is unavailable during your US business hours creates real problems when your CPA needs a document corrected before a filing deadline, or when your bank flags a transaction that needs same-day classification. Timezone overlap is not a soft preference — it's a compliance risk when deadlines are involved.

Nearshore virtual bookkeepers based in Latin America work your business hours — Eastern, Central, Mountain, or Pacific — and are reachable by Slack, Zoom, or phone the same moment your CPA sends a question. They speak English at an 8/10+ proficiency standard (Rose's published screening floor), which means communication with your accounting team is clear and fast. According to SHRM's Global Workforce research (2023), communication barriers and timezone misalignment are the top two reasons companies discontinue offshore professional services arrangements.

Every Rose team member also ships with a role-specific AI copilot trained on their software — so a bookkeeper placed with you arrives already proficient in QuickBooks, Xero, or whichever platform your business runs. That's not generic ChatGPT access; it's a tool calibrated to your exact workflow. Learn more about how that works on our AI advantage page.

Nearshore Virtual Bookkeeper (Latin America)

- Works US business hours — same real-time availability as an in-house hire

- English fluency at 8/10+ — no communication friction with your CPA or bank

- Trained on US GAAP and IRS-standard expense categories

- AI copilot pre-trained on QuickBooks, Xero, and FreshBooks workflows

- Flat $2,500/mo — recruiting, HR, and payroll included

Offshore Virtual Bookkeeper (India/Philippines)

- 6–13 hour timezone gap — async by default, slow on deadline days

- Variable English fluency — miscommunications on chart-of-accounts setup are common

- May use different accounting standards (IFRS vs. US GAAP)

- Recruiting, onboarding, and management burden falls on you

- Lower hourly rate but hidden costs in rework and oversight time

How to Set Up Your Virtual Bookkeeper for a Smooth Tax Filing in 2026

Hiring the right bookkeeper is step one. The bigger leverage is in how you set them up from day one. The following process is what Rose recommends for clients whose primary goal is clean year-end books that make tax filing fast.

Define Your Chart of Accounts Together

Before your bookkeeper touches a single transaction, sit down with your CPA and your new bookkeeper to align on the chart of accounts. This 60-minute meeting eliminates the most common source of year-end rework — miscategorized expenses that your CPA has to correct at $200/hr.

Establish a Weekly Reconciliation Cadence

Weekly reconciliation means tax season is 52 small check-ins rather than one enormous scramble. Ask your bookkeeper to deliver a reconciled transaction report every Friday so nothing ages more than seven days.

Build a 1099 Vendor Tracker from Day One

Have your bookkeeper create a vendor tracking spreadsheet in January — not November. Collect W-9s from every contractor over $600 in real time so you're never chasing vendors in January for tax documents due January 31.

Schedule a Q3 Tax Planning Meeting

By September, your bookkeeper should have nine months of clean P&L data ready. Share it with your CPA in a Q3 planning call so you can make estimated tax adjustments, accelerate deductions, or plan equipment purchases before December 31 — when there's still time to act.

Deliver a Year-End Close Package

In January, your bookkeeper produces the full year-end close package — reconciled statements, P&L, balance sheet, fixed asset schedule, and 1099 vendor list — and delivers it directly to your CPA. Your CPA's job at that point is pure tax strategy and filing. No cleanup, no reconstruction.

If your business has complex accounts payable workflows — multiple vendors, recurring invoices, early-payment discounts — it's worth reading our overview of the best accounts payable virtual assistant services to understand how a dedicated AP specialist can work alongside your bookkeeper to keep the vendor side of your books spotless going into tax season.

According to QuickBooks Small Business Insights (2023), small businesses that maintain monthly reconciled books pay an average of 28% less in year-end accounting fees than businesses that hand their CPA a full year of uncategorized data. That's a direct, measurable return on your bookkeeping investment.

What to Look for When Hiring a Virtual Bookkeeper for Tax Support in 2026

Not every virtual bookkeeper is equipped to handle the tax-adjacent work described above. Here are the specific qualifications worth screening for when your primary need is tax-ready books:

- US GAAP familiarity — they should know the difference between cash and accrual basis and be able to explain which one your business uses and why

- IRS expense category knowledge — specifically Schedule C (sole proprietors), Schedule E (rental income), or Form 1120-S (S-Corp) depending on your entity type

- 1099 experience — have they managed contractor tracking and year-end 1099 prep before? Ask for a specific example.

- CPA-ready deliverables — can they produce a clean year-end close package? Ask what that package includes and how they format it.

- Software proficiency — QuickBooks Online, Xero, or whatever platform your CPA prefers for import

At Rose Talent Solutions, every bookkeeper placed through our bookkeeping and accounting service is vetted against these criteria before they ever reach a client. The placement process typically takes about seven days from your intake call to your first working session. And if the fit isn't right, we replace your team member at no additional cost — that's the only guarantee we offer, and it's the one that matters most. When you're ready, you can get started here.

According to Gallup's State of the Global Workplace (2023), remote workers in time-zone-aligned roles report 23% higher engagement and productivity scores than those working asynchronously across large timezone gaps — a finding that translates directly to bookkeeping accuracy and responsiveness on your team.